{kind=link}

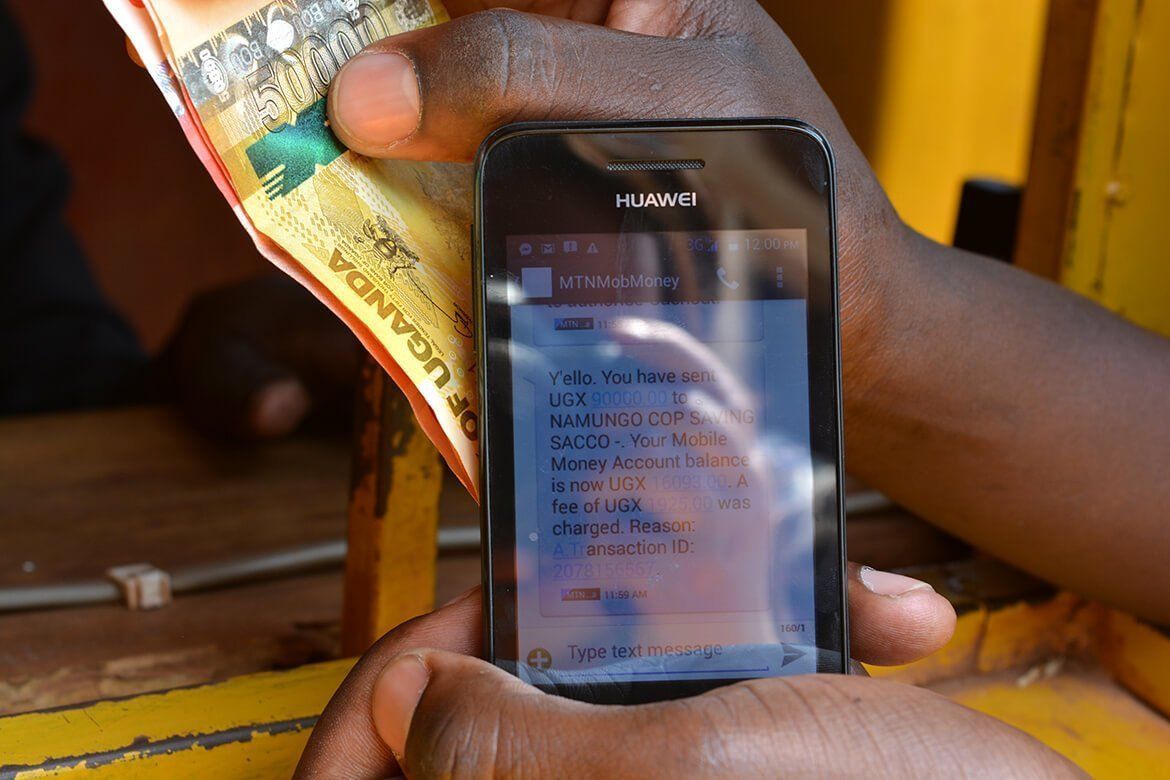

Uganda stands at a fascinating crossroads in its financial evolution. On one hand, the country boasts one of the most vibrant mobile money ecosystems in Africa, with 36.7 million active wallets processing over UGX 390 trillion in transactions annually as of mid-2026. Platforms like MTN MoMo have transformed how millions of Ugandans send money, pay bills, and even access basic credit.

Yet, despite this impressive foundation and aggressive policy pushes from the Bank of Uganda toward a cash-lite future, a true digital money economy where electronic transactions dominate everyday commerce, merchant payments, savings, lending, and even high-value deals remains elusive.

Large segments of the population and economy still cling to cash, and recent regulatory moves have sparked fresh debate about whether ambition is outpacing reality.

The latest flashpoint came when a circular from the Bank of Uganda (EEDNPS.306.2, dated May 29) announced sharp reductions in interbank cheque limits and new over-the-counter cash withdrawal caps, set to take effect on January 1, 2027.

Individuals will be limited to UGX 50 million daily and UGX 250 million weekly, while corporates face UGX 500 million daily and UGX 2.5 billion weekly. The central bank framed these measures as essential steps to promote electronic channels, reduce the costs of printing and handling cash, and build a more transparent, modern financial system.

Supporters argue that such limits will curb illicit flows and encourage innovation. Critics, however, see them as tone-deaf to the realities of Uganda’s informal, cash-heavy economy.

The ground reality

Imagine a small town with a bustling cattle market, a single buyer might purchase over 100 cows in one day, a transaction easily exceeding the new daily cap for individuals.

The nearest bank sits 40 kilometers away, with unreliable roads and limited digital infrastructure. For many traders in agriculture, livestock, construction, and wholesale markets, cash remains not just convenient but practically necessary. These businessmen handle daily cash flows far above UGX 50 million, yet operate in environments where digital alternatives are not yet seamless or trustworthy.

This anecdote is not an isolated complaint. It reflects a deeper structural mismatch. Uganda’s economy is still predominantly informal, with a vast rural population engaged in agriculture and small-scale trade. While urban centers like Kampala and Entebbe enjoy relatively better banking density and connectivity, much of the country does not.

Policies designed in air-conditioned boardrooms in the capital can feel disconnected when applied to villages where electricity is sporadic, internet is expensive or absent, and trust in digital systems is low. The circular’s requirement for banks to profile cash-heavy sectors and justify large withdrawals only adds layers of bureaucracy that small players may struggle to navigate.

The last mile problem

At the heart of Uganda’s digital money challenges lies a persistent infrastructure gap, particularly between urban and rural areas. Internet penetration remains uneven, with usage significantly higher in cities than in the countryside.

Reliable electricity is another major constraint; rural electrification rates hover in the low double digits in many regions, making consistent phone charging, agent operations, or even basic digital transactions difficult. Without dependable power and network coverage, mobile money agents often run out of float, networks go down during critical market days, and users lose confidence in the system.

Smartphone ownership and affordable data further complicate the picture. While mobile money has succeeded partly because it works on basic feature phones, advancing to fuller digital financial services such as merchant payments, digital credit scoring, or online commerce requires more advanced devices and reliable connectivity.

High data costs relative to incomes deter many from exploring beyond simple person-to-person transfers. In rural markets, where most economic activity occurs, these barriers mean cash continues to feel safer, faster, and more familiar.

Literacy, trust, and cultural preferences

Even where infrastructure exists, low digital and financial literacy creates another formidable obstacle. Many Ugandans, especially older generations, women in rural areas, and those in informal sectors, lack the confidence or knowledge to navigate advanced digital tools.

Fraud and scams have eroded trust. Stories of lost savings due to phishing, unauthorized deductions, or system glitches circulate widely, reinforcing a preference for the tangibility of cash. Unlike physical money, digital errors can be harder to reverse, and in a country where personal relationships often underpin business deals, the human element of handing over notes carries reassurance that screens cannot yet replicate.

Gender and generational divides compound these issues. Women, who form a large part of agricultural and small trading activities, often face additional hurdles in obtaining national IDs required for full KYC compliance or accessing certain services. Youth may be more tech-savvy but still encounter barriers in scaling up digital credit or savings due to limited formal financial histories.

When digital money feels more expensive

Paradoxically, while digital payments promise lower long-term costs for the economy, they can feel more expensive for everyday users. Mobile money transaction fees, combined with the 0.5% excise duty on withdrawals introduced in previous years, have at times discouraged usage.

In informal markets, cash transactions often incur no explicit fees, making them attractive despite risks like theft or counterfeiting. High-value deals in real estate, livestock, or construction frequently involve large cash bundles because parties perceive digital channels as costly, slow, or prone to scrutiny.

Past policy experiments, such as earlier mobile money taxes, demonstrated how sensitive the sector is to cost changes; transaction volumes dropped sharply before recovering. The new cash caps risk repeating this pattern if digital alternatives are not made demonstrably cheaper and more convenient first.

Regulatory ambition versus practical readiness

The Bank of Uganda deserves credit for its vision. The National Payments System and e-payments strategy aim to create a cash-lite economy that enhances efficiency, deepens financial inclusion, and supports broader economic growth. Interoperability improvements and agent banking expansions have already brought services closer to people.

However, top-down mandates like the 2027 caps can feel premature when foundational elements, widespread merchant acceptance, robust rural infrastructure, affordable services, and public trust are not fully in place. Public reaction to the circular, with many echoing the cattle market example, highlights a communication and consultation gap. Policies perceived as punitive rather than enabling generate resistance rather than adoption.

In contrast, successful digital shifts in other markets have often involved heavy investment in incentives, education campaigns, and phased implementation that aligns with ground realities.

The road ahead

Uganda has already achieved remarkable progress. Mobile money has brought millions into the formal financial fold, powering remittances, small business growth, and resilience during crises like COVID-19. The projected growth of the mobile money market, with strong CAGRs forecast into the 2030s, shows the potential is real.

To overcome the deterrents, a more balanced approach is needed. This includes accelerating rural electrification and internet expansion, subsidizing data or devices in underserved areas, intensifying financial literacy programs tailored to different demographics, and reviewing transaction costs to make digital genuinely competitive with cash.

Strengthening cybersecurity, consumer protection, and merchant onboarding will build trust. Phased implementation of caps, with exemptions or higher thresholds for documented high-cash sectors like agriculture, could prevent economic disruption while still steering toward digitization.

Ultimately, achieving a genuine digital money economy in Uganda requires more than regulations; it demands empathy for how ordinary Ugandans, from Kampala traders to upcountry cattle buyers, actually live and work.

By addressing infrastructure, affordability, literacy, and trust head-on, while tempering ambition with practicality, the country can transform its impressive mobile money foundation into a truly inclusive, efficient, and modern financial system. The journey will not be quick or easy, but getting the balance right could unlock significant economic potential for generations to come.